Publised on May 2, 2026

What Is a Bankability Score and Why Does Your Lender Care?

If your enterprise has ever been denied a commercial loan, a line of credit, or equipment financing without receiving a transparent explanation, you are not alone. Most operators assume that lenders evaluate a business based purely on top-line revenue or time in business. While those metrics matter, they are rarely the deciding factor.

Commercial institutions make credit decisions based on a highly specific matrix of underwriting benchmarks that dictate your Bankability Score. If your core financial statements do not meet these structural thresholds, your application is frequently flagged and declined by automated credit risk models before an underwriter ever reviews your narrative.

To protect your capital runway and ensure your business can fund its next phase of infrastructure growth, you must actively manage the three primary metrics lenders prioritize.

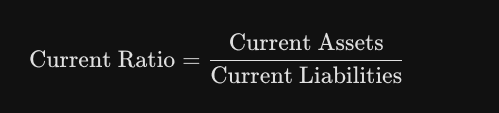

1. The Liquidity Test: Current Ratio

Lenders use this metric to evaluate your organization's short-term financial resilience. It measures whether your business possesses enough liquid runway to extinguish its immediate obligations over the next twelve months.

The Threshold: Lenders look for a benchmark of 1.0$\times$ to 1.5$\times$ or higher. A ratio below 1.0$\times$ indicates that your short-term liabilities exceed your cash and near-cash assets. To a lender, this represents immediate working capital stress and an elevated default risk.

2. The Debt Capacity Test: Debt Service Coverage Ratio (DSCR)

The DSCR is arguably the single most critical metric in commercial underwriting. It quantifies your enterprise's capability to comfortably generate enough operational cash flow to service your existing debt obligations alongside the new loan payments you are requesting.

The Threshold: Institutional standard thresholds typically mandate a DSCR of 1.25$\times$ or higher. A ratio below this ceiling indicates that your net operating cash flow is too tightly leveraged to absorb sudden market volatility or freight and labor adjustments.

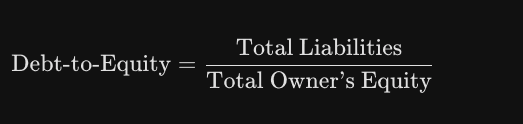

3. The Leverage Test: Debt-to-Equity Ratio

This ratio measures your company's capital structure. It illustrates how much of your business engine is sustained by institutional leverage versus the actual equity or retained earnings invested by the ownership.

The Threshold: Underwriters generally want to see this ratio maintained below 2.0$\times$. A metric scaling higher than 2.0$\times$ indicates that the enterprise is highly leveraged, signaling to lenders that outside creditors hold a greater financial stake in your operational infrastructure than you do.

Audit Your Asset Portfolio: The Bankability Scale

Before you schedule an evaluation with a commercial lender, grade your balance sheet against these institutional baselines:

Tier Grade | Matrix Performance | Underwriting Position |

Grade A | All three metrics comfortably exceed thresholds. | Highly bankable; premium credit terms and optimal rates. |

Grade B | Two metrics pass baseline requirements. | Conditional approval likely; expect restrictive covenants or higher pricing. |

Grade C | Only one metric meets minimum compliance. | High risk; structural financial adjustments required prior to filing. |

Grade F | Zero metrics pass institutional thresholds. | Fundamental restructuring required; clear capital deployment changes needed. |

Designing the Solution

The strategic advantage of these formulas is that they are not static. Every single variable inside your Bankability Score can be intentionally engineered and optimized:

Accelerating your accounts receivable turnover directly improves your Current Ratio.

Auditing operational overhead and eliminating margin leaks instantly expands your Net Operating Income, maximizing your DSCR.

Retaining net earnings or strategically restructured debt notes rapidly rebalances your Debt-to-Equity ratio.

Most corporate operators remain completely blind to these numbers until they receive a formal rejection letter from their bank.

We don't believe in running an enterprise through guesswork. Measuring, diagnosing, and optimizing your Bankability Score is a foundational component of every Financial Physical we conduct. By treating your balance sheet as an intentional piece of corporate infrastructure, you can confidently secure the institutional capital required to fund your long-term ambitions.